A lot of people are surprised when I tell them I use credit cards almost exclusively. I think that reaction highlights one of the biggest misconceptions about credit cards.

When I was younger, I viewed credit cards as a way to buy things I couldn’t comfortably afford. I would often open store-branded cards with promotional interest rates and make purchases that I then paid off over time. Looking back, I at least understood one important thing: credit cards can be dangerous. Because of that, I generally tried to avoid them whenever possible.

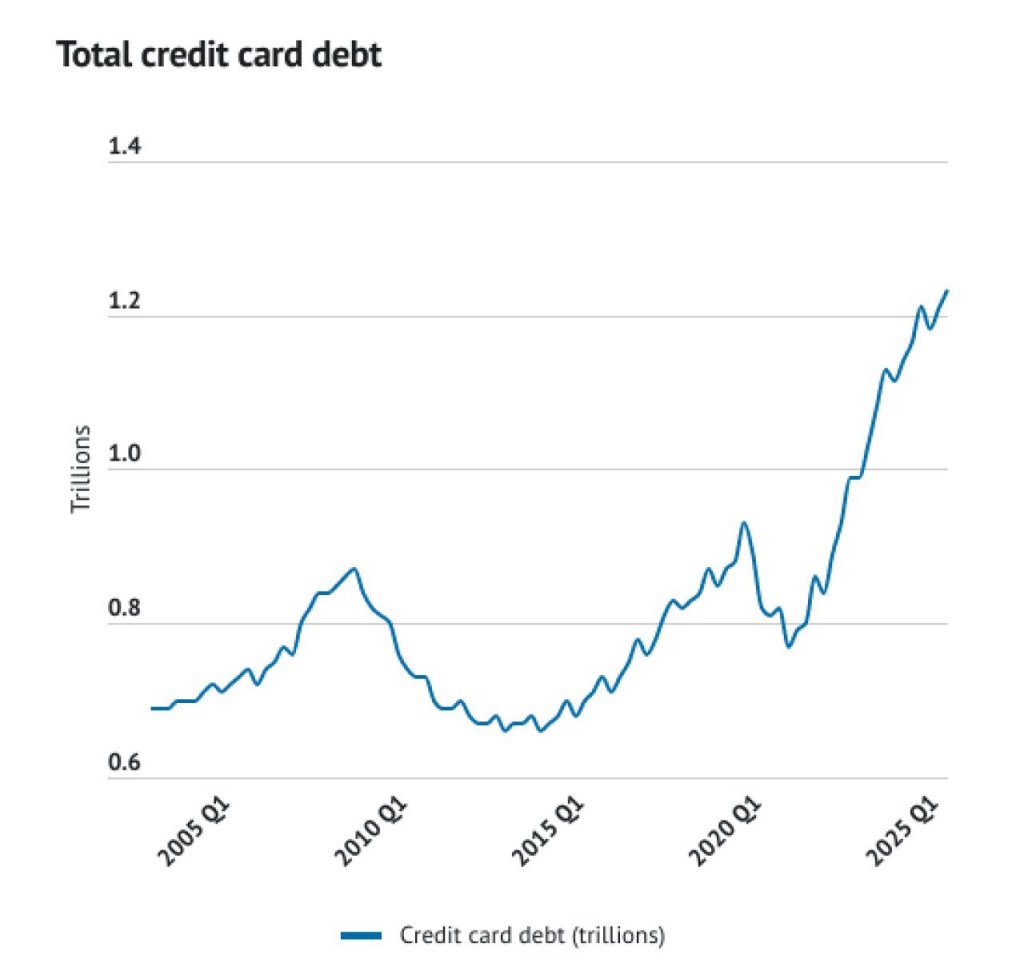

That’s still a pretty good way to think about it for many folks. Right now, Americans owe about $1.25 trillion in credit card debt, and the number of people who’re late on their payments is up to its highest point in years. In fact, the rate of people who’re 90 days or more behind on their credit debt is 13.14%, which is the highest in 15 years. With housing costs going up, groceries getting pricier, insurance premiums climbing, and cars now often averaging $50,000 or more, many families are finding it tough to make ends meet.

But the problem isn’t the credit card itself. The problem is using a credit card as a substitute for cash you don’t actually have.

That’s exactly how I used them when I was younger. Today, I use them very differently.

Mindset Shift

I track my expenses down to the penny. Every dollar that comes in and every dollar that goes out is accounted for, much like a business tracks its cash flow.

Once I became proficient at doing this, I realized something important: it didn’t really matter whether I used cash, a debit card, or a credit card for my everyday purchases. What mattered was that I consistently spent less than I earned.

That realization changed how I viewed credit cards. Instead of using them to finance purchases I couldn’t comfortably afford, I began using them as a payment tool for expenses I was already going to incur. Groceries, gas, insurance, utilities, travel—expenses that were already part of my budget.

At that point, the benefits became obvious. If I was going to spend the money anyway, why not earn cash back or travel rewards in the process?

So I dove in. Today I use a rotation of three to four credit cards, each optimized for different spending categories. The result has been thousands of dollars in rewards over the years. As I write this, my accumulated cash back balance alone stands at $13,704.

The key difference is that I never view my credit limit as spending power. The credit card is simply the vehicle. The budget is still what determines how much I can afford to spend.

Every time I open a new credit card, I follow the same routine.

First, I adjust the notification settings so I’m alerted whenever a purchase is made and whenever a payment is received. Next, I set the account to automatically pay the full statement balance every month. Finally, I sync the card to the software I use to track my spending.

After that, there’s really nothing left to do.

The credit card simply becomes another account flowing through my financial system. Every purchase is tracked, every dollar is accounted for, and every payment is automated.

My only job is to remain cash-flow positive. As long as I’m consistently spending less than I earn, the statement balance will be paid in full and on time every month.

I do pay attention to credit limits and account balances. While I never view my credit limit as permission to spend, I try to avoid allowing balances to climb too high relative to the available credit. High utilization ratios can temporarily lower your credit score, even when you pay your cards in full.

The way I see it, responsible credit card use isn’t about willpower. It’s about having a system. Once the system is in place, the rewards, fraud protection, and convenience become benefits rather than temptations.

The Most Important Takeaway

If you take anything away from this article, take a few minutes to think about how you view and use credit cards.

How do they fit into your financial routine?

Do they cover cash flow shortfalls when money is tight? Are they used to finance purchases you can’t comfortably afford? Do they pay for vacations that will take months or years to pay off?

These are important questions because credit cards can either be a useful financial tool or an expensive financial burden. With interest rates commonly exceeding 20%, carrying a balance can quickly erase any rewards, points, or cash back you earn.

My advice is simple: become proficient at managing your cash flow. Know your income, expenses, and spending habits as well as a business owner knows the finances of their company. When you understand where every dollar is going, the payment method becomes much less important.

At that point, a credit card can be treated much like a debit card—simply a tool used to facilitate purchases you were already planning to make.

Set up account alerts. Automate payments. Track your spending. Pay the full statement balance every month.

When used this way, credit cards can provide convenience, fraud protection, cash back, and travel rewards without costing you a penny in interest.

The secret isn’t finding the perfect credit card. It’s building a financial system that allows you to use any credit card responsibly and beat credit card companies at their own game.

Leave a comment