When the news says, “The Federal Reserve raised interest rates today,” most people tune it out. It sounds like something that only matters to Wall Street.

But the truth is, the Fed’s interest rate affects almost every part of your financial life—from how much you pay each month to what your house and investments are worth. Understanding how interest rates work gives you an edge most people don’t have. It helps explain why mortgages suddenly become expensive, why stock markets swing wildly, and why housing prices rise and fall.

Let’s break it down in plain English.

What Interest Rate Does the Fed Control? The Fed controls something called the federal funds rate. This is the interest rate banks charge each other for overnight loans. At the end of every business day, banks have to meet legal reserve requirements. Some banks end the day with too much cash, and some end the day a little short.

So they do what humans do: they help each other out. Banks with extra money lend it overnight to banks that need it. This is called the federal funds market. The Fed (Federal Reserve) sets a target range for this rate because it becomes the base price of money for the entire economy.

Think of it like this:

If it’s cheap for banks to borrow money → it becomes cheap for everyone else. If it’s expensive for banks to borrow money → it becomes expensive for everyone else

Why overnight?

Because banks are constantly moving money in and out as customers deposit, withdraw, swipe cards, and pay bills. Overnight lending keeps the whole system stable and liquid so banks can operate smoothly the next day.

That may sound technical, but it becomes the foundation for nearly every other interest rate in the economy, including: mortgage rates, credit cards, auto loans and business credit. Think of it like the thermostat for the economy. When the Fed raises rates, spending cools down. When the Fed lowers rates, spending heats up.

How Fed Interest Rates Affect Consumer Costs

When interest rates are low, borrowing money feels easier: mortgage payments are smaller, car loans cost less, credit card interest is more manageable, businesses borrow and hire more. Life feels smoother.

The Fed lowers rates when they feel the economy may be struggling and want to give it some juice.

When interest rates rise, the opposite happens. The Fed raises rates mainly to fight inflation. It’s their way of saying, “Let’s slow spending down before prices spiral out of control.”

How Interest Rates Affect Asset Values

While most of us are aware of how interest rates affect us as consumers who use credit, it’s less known how they affect asset values.

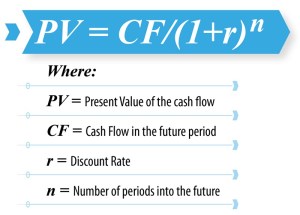

How much is future income worth today? This is a concept taught at every business school around the world called Present Value of Future Cash Flow.

Interest rates don’t just change what you pay. They also change what things are worth. Stocks, real estate, and businesses are valued based on the money they are expected to produce in the future.

This is the most important idea in investing, and almost no one explains it in plain English. Assets— like stocks, rental properties, and businesses, are worth money because they produce future cash. A stock pays dividends. A rental property produces rent. A business generates profits.

But here’s the question investors always ask:

If I was all knowing how much cash a business would generate over the next decade or so, how much would I be willing to pay today for those future earnings?

That’s called Present Value.

And interest rates are what determine the answer.

A Simple Example, would you rather have:

$1,000 today or $1,000 ten years from now?

Obviously today because you could invest it. Not to mention inflation will reduce its buying power over time. So future money is always worth less than money held today. Interest rates tell us how much less.

When Interest Rates Are Low:

When interest rates are low, it’s not as appealing to wait for a return. Because the future money isn’t discounted much, investors are happy to pay more today for the promise of future income. This drives up prices for any asset that generates income. For example, if a company could earn $1 million in profits over ten years, and interest rates were 1%, you’d need a significant amount of money invested at that rate to achieve that same million in ten years. So, the present value of that future income is considered more valuable.

What Happens When Rates Are High

When interest rates are high, keeping your money in safe investments can be a smart move and can even yield good returns. But here’s the thing: when you’re looking at future money, it’s often worth less than it seems. That’s because investors are happy to pay a bit less today for the income they’ll get later. For instance, if the Federal Reserve bumped interest rates to 15%, any asset that made money would be worth a lot less. Basically, if you knew exactly how much cash an asset would bring in over the next ten years, at 15% interest, you’d need a lot less money in a safer investment today to get the same amount in the future. So, in short, future money is worth less.

This is why markets react so strongly to Fed announcements. Even small rate changes can shift trillions of dollars in asset values.

Why the Fed Must Stay Independent

Because of its power, the Federal Reserve was designed to be independent from politics. If presidents controlled interest rates, there would be constant pressure to keep them low—boosting stock markets, creating short-term job growth, and making borrowing cheaper for consumers. That looks great in the moment, but keeping rates too low for too long can lead to inflation, asset bubbles, and painful economic crashes later.

Recently, there has been public pressure on the current Fed chair, Jerome Powell, to act in ways that support political goals. Politics aside, this is exactly why independence matters. The Fed must be able to make unpopular decisions when necessary and focus on long-term economic stability—not short-term political wins. A stable economy depends on a central bank that can say “no,” even when that’s not what leaders want to hear.

The Big Takeaway

The next time you hear, “The Fed raised interest rates by 0.25%,” don’t think of it as an abstract economic headline.

That small number affects:

Your mortgage payment, your credit card bill, your retirement account, the housing market, job growth & Business investment.

It’s not just a finance story.

It’s a personal finance story.

And once you understand how interest rates work, you stop reacting emotionally and start making smarter long-term decisions with your money.

Leave a comment