One of the most common phrases in personal finance sounds responsible on the surface: “Can we afford it?” But I think that question is incomplete.

A better question is: “Should we afford it?”

Because those two questions can lead to very different outcomes.

“Can we afford it?” is a math question

“Should we afford it?” is a life question

When we ask can we afford something, we’re usually just checking one thing: Do I have the money right now, or can I cover the required payment monthly? If the answer is yes, we feel justified. Swipe the card. Sign the contract. Move on.

But that ignores everything else:

• What else that money could be doing?

• How this decision affects your cash flow?

• How it affects your future financial goals?

• How would your future self react to the purchase?

You may be able to afford it…but should you?

The Trap of Living at Zero Cash Flow

It’s easy to end up with no cash flow, and it’s something we should all be mindful of, both now and moving forward. Think of it as every dollar being already committed to things like car payments, subscriptions, new furniture, a larger home, or, even worse, credit card bills.

On paper, everything is “affordable.” In reality, there’s no breathing room. Any surprise becomes a crisis. Any opportunity feels impossible. That’s not wealth. That’s financial fragility dressed up as comfort.

Cash flow flexibility = Real Freedom

It turns out, what most folks really crave isn’t just more stuff. Instead, they’re looking for less stress, more options, and a bit more breathing room—all of which can lead to a more peaceful life. This is all about having the freedom to handle things as they come, thanks to steady cash flow.

Cash flow flexibility means: You can handle emergencies without panic. You can invest when opportunities appear. You can say yes to meaningful things & you can say no to things that don’t matter

To really make cash flow flexible, you need to be intentional and disciplined. It’s about having the right mindset to confidently say either, “We can afford it,” or “We don’t need it.” This mindset shift can truly change everything.

Next time you’re tempted to buy something, try reframing the question to force your brain to think about it differently.

Instead of: “Can we afford this?” Ask: “Does this move us closer to or farther from our future goals?” Or: “What am I giving up by saying yes to this?”

Suddenly spending becomes intentional instead of automatic.

A Personal Example

I have a general picture of what I want my financial life to look like in the future. I don’t focus on one exact number — I think in terms of a range of reasonableness that gives me security and flexibility.

From there, I work backward.

Right now, that means aiming to:

• Invest about $50,000 per year

• Save about $5,000 per year in a HYSA for emergencies and other big expenses

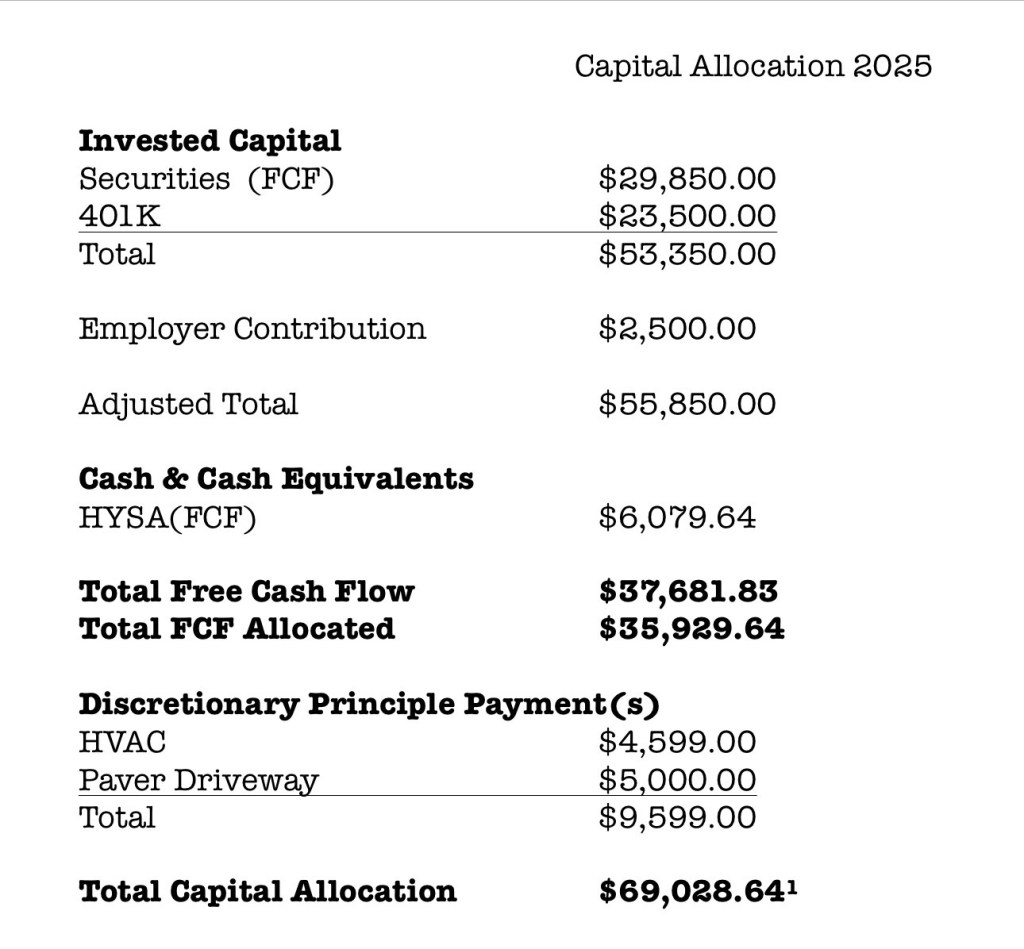

I’ve shown this page before, but it really fits with this post too. I’m not too hard on myself about hitting the yearly goals. Sometimes it’s more, sometimes it’s less. In 2025, I actually saved more than I expected, which was fantastic. But I’m not going to spend just for fun. However, if I want something and my goals are met, I usually treat myself. Usually, my splurges happen after I’ve hit my goals or I’m almost there. So, usually, it’s around the end of the year.

For example, 2025 was a solid year so as a reward, I upgraded my Garmin watch to the next level and my Apple AirPods to the 3rd gen. That came to a total of $1,122.27. I was able to sell my old devices for $465.00 and get a 10% Rakuten cash back. So, overall, it wasn’t a huge splurge; my actual expense was only $572.27. But the point is, I was intentional. It wasn’t random. And it happened only after my goals were met.

My long-term goal is to be free of consumer debt and only carry mortgages on rental properties. So if I finance something along the way, any extra cash flow goes toward paying it off aggressively. Which is what you see at the bottom under Discretionary Principle Payments

I’ve been incredibly lucky! It’s not all about luck, though—there’s been a lot of discipline and hard work too. But decisions were made, and now I’m blessed with very healthy cash flow flexibility. But that wouldn’t be the case if I only asked, “Can I afford it?” before making financial decisions.

Alignment beats affordability

The goal of personal finance isn’t to squeeze every dollar until nothing is left. The goal is to build a life where: Your spending matches your values, your money supports your future & you have room to breathe. When you shift from can we afford it to should we afford it, spending becomes a tool instead of a trap.

This idea isn’t new. Long before budgeting apps and financial gurus, Stephen R. Covey captured the same principle in a simple phrase: begin with the end in mind. If we know what kind of future we want, today’s spending decisions start to look very different. The question is no longer just “can I pay for this?” but “does this help me build the life I actually want?”

Affordability vs. intentionality

Covey’s habit reminds us that effectiveness isn’t about doing more. It’s about doing what matters. The same is true with money. You can afford many things. But you should only afford the things that support the future you’re trying to create. This is how spending turns from impulse into intention.

Of course, things aren’t set in stone. There will be times when spending gets a little too high, and that’s totally okay. As long as you eventually get things back in check and refocus. After all, you’re aiming for a good batting average over time. There will be some slow periods, strikeouts, and pop-outs, but that doesn’t mean you have to change your goals or how you play. It’s just part of the game.

Final thought

You don’t need to live like a monk. You don’t need to say no to everything. But you do need to protect your cash flow like it matters — because it does.

In a highly consumer driven economy there is a ton of both money and effort expended to get you to spend your hard earned money & you may be able to afford it.

But the better question is:

Should you?

Leave a comment