This has been a very busy year so far. I took a week cruise, had a pretty lengthy rental vacancy, bought a car and did some home projects at my primary house. Now that things are finally settling down, I’ve begun to take stock of where I am in life and the pivotal moments that altered my course in getting here. In this reflective mood, I was searching for the biggest contributor to the path I am currently on. A path I hope leads to fulfillment and early retirement. Surely I wasn’t on this path in high school or my college years. So what changed?

I’ll tell you what changed..I read a really big book. I’ll never forget when I came across the book that changed my life forever. It was right around the time when Borders the book store was going out of business and they had their inventory in the parking lot under huge tents. But first a little back story to set the table.

Admittedly, I mainly went to the book store to look at the music selection they offered or to get coffee, never much of a reader as a kid. Although I liked the idea of reading, I could never find anything to keep my interest for more than a few pages. I often had to re read the same paragraph over and over to comprehend information. Comprehension in school was always a weak subject for me. I struggled. It all seemed so boring. Comprehending what I was reading took real work. Brain work. I used to think I had a reading disability to be honest. I can recall finishing only one book as a kid, although the name of it slips my memory. Still, the idea to step into a different world, or to see the world through someone else’s paradigm was intriguing. An Introvert at heart, I pined for the ability to read, learn and discover new things. But what would interest me enough to focus my mind? This always eluded me growing up.

So I moved back to the town I grew up in June of 2007 shortly after graduating college in May of that year. I was lost to say the least. At that time I remember being so confused on who I was. What was I passionate about? What was I good at, if anything at all? I always admired those friends I grew up with who knew exactly what they were passionate about and wanted to do with their lives. I just had no idea. It was worrisome and gave me great anxiety at this time of my life to be honest. I was an average student at best, who never really applied myself and was hardly interested at all in basically any subject matter that was taught in school. This also worried me. I was craving something to be passionate about. Oddly, although I had no real passions, I always knew if I found something I cared about I would be relentless and good at it. I can get obsessed with something if I care enough.

After a few months living back home I got a job as a Nuclear Security Officer. What was intended as a transition job turned out to be a pretty good job with excellent pay and benefits. And although I had no real passions at the time, I did love the idea of being financially independent.

I can’t put my finger on exactly when the interest was piqued. I will say that my hire date was October 1st 2007, the peak of the housing financial crisis. And the town I live in was hit exceptionally hard with home prices dropping far more than national averages. Taken together, with a job that was paying me real money at a young age, I smelled a huge opportunity. Rock bottom interest rates, home prices off 60%, stocks dirt cheap, huge pay gains, no debt, living at home, no kids and somewhat ambitious. Collectively these were a set of variables that if harnessed correctly could set me up for life. I knew very little at the time, but I did see this incredible opportunity and viewed it as a once in a generation type event. This opportunity ignited a strong interest. Still, at this point I wouldn’t quite call it a passion. Nonetheless, I began devouring anything I could get my hands on that had to do with getting rich. I read everything. Although I truly believe every book I read was an important developmental piece of my story, not one book changed me like the one I was soon to find.

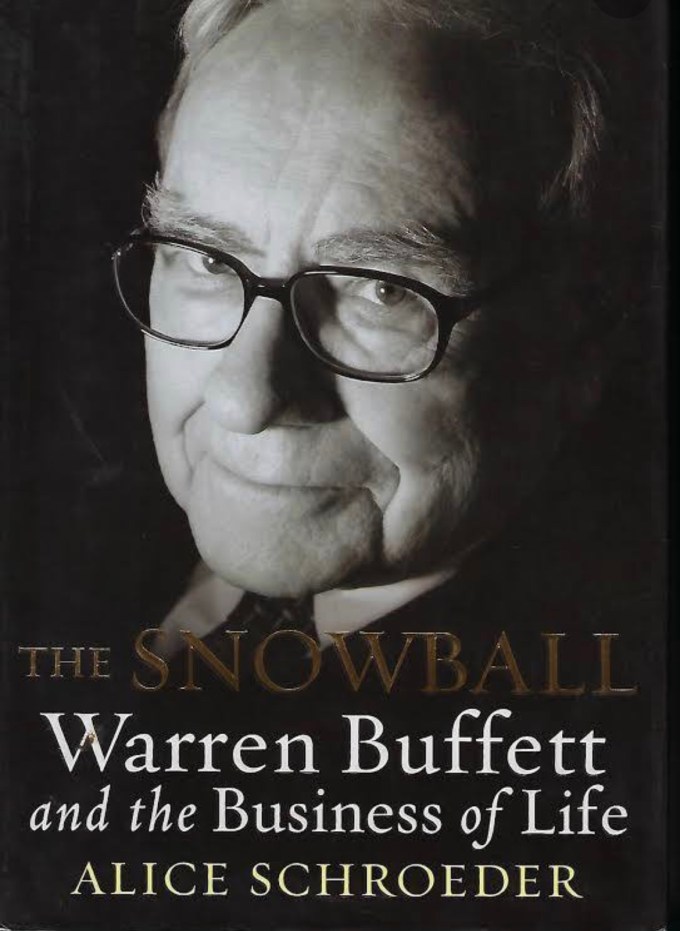

Sometime around 2010 during the bankruptcy process for Borders I found The Book. In the parking lot of the mall was all of Borders’ inventory under these huge tents. Rows and rows of books. I came across one book of this old wise looking guy. The look on his face was one that said, I know more than you. The book was The Snowball Warren Buffett and the Business of Life. Embarrassingly, I had never heard of Warren Buffett. And why this book intrigued me to this day I have no idea. It was a massive book with 787 pages of fine print and minimal pictures. The idea of ever reading it seemed daunting. But I had been reading about investing for a few years and the book was cheap so I figured what the hell. I remember reading the summary on the inside and phrases like the “Oracle of Omaha” and the “Sage of Nebraska” jumped out at me. As if he were some type of living legend. And for some reason the description of him as just a plain and simple ordinary billionaire is what sold me. I had to know who this guy was.

And so it began. I devoured that book. And it sparked a passion for business and investing that still fascinates me today.

Buffett’s story is relatable in many ways. You read about other billionaires and most if not all started a hugely successful company. In other words they created something. And while inspiring and interesting to read, it does often leave one feeling inferior. However, Buffett didn’t create anything. He is the ultimate capitalist. I don’t have the time to write out his biography in this post, but I encourage you to read his story or watch some of the biographies that have been done on him.

To summarize, he graduated from high school with roughly ten thousand bucks, invested in companies ran by others and ultimately became the richest person in the world. He takes the long view, understands value and is a brilliant investor. Some of his investments have been in plain sight, yet somehow he saw value where others missed it. Many of his investments he has owned for decades. In other words, he shuns the short term mentality that grips Wall Street. Oh, and he still lives in the same upper middle class house he bought in 1956 for $31,500. Intrigued?

You may be asking, ok but why did this book change my life? When I was younger, I can’t say I had passions, but I was incredibly curious. I would ask random questions like “I wonder how much money this store makes?” Needless to say, although I was curious about many things, I had a particular curiosity about business. I always fantasized about being a business owner and how pleasurable it must be to be in control and work with the numbers, alone at night in your office. The idea of working with “my numbers” intrigued me. Something I can have control of, optimize and compete in. I don’t think I thought of it as a passion at the time. But this book unlocked that passion.

Buffett’s approach is to buy pieces of companies in the stock market. And to approach those pieces as if you were buying the whole company. Berkshire Hathaway, which Buffett is a controlling shareholder, also owns wholly owned companies. And in these wholly owned companies he leaves the management in place. Essentially he writes a check to buy either a piece or the whole company, and says I want to buy the management too, just send me whatever excess capital you don’t need in your business. This is very different than the typical corporate raiders, or day trading masses that populate Wall Street. Buffett’s approach therefore is not of a speculative nature but that of an owner. What this taught me is I don’t have to have big bucks and or creativity to start a company of my own, I can save money and buy little pieces of companies via the Stock Market. And my approach can be the same. I can check in every quarter and see how my company is doing by reading the quarterly reports. In essence I would get to live out that childhood fantasy. Suddenly a whole new world opened up. But I had no idea early on how to read accounting statements or what makes a good business. Why did some companies fail? Or What made an exceptional company? But the passion was born. And to this day this mindset shift has paid dividends, pun intended.