I love stocks. Anyone that knows me knows this. It’s a true and natural love. Unconditional. The reason for this, 1) I view them as owning a piece of American business. 2) I recognize that they will be the gift that keeps on giving. 3) It is really a lazy asset class, meaning I don’t need to do anything and 4) I don’t need to know anything either. You may be wondering how can that be? You don’t need to do or know anything?! Yes. That’s the magic of the stock market. In fact, I often make the case that this is why they are my favorite asset class. I can let the best CEO’s in the world run them and I can just sit back and enjoy the ride. What you need it discipline to keep buying. And to be educated on want you really own. This education should breed confidence. So I guess I lied a tad. But you can certainly get all the education you will need to be successful from this blog. Anything more is probably unnecessary.

Owning a stock is very much like being a silent partner in a company. The company needed your capital to grow. In exchange for your capital, you are a part owner. If you picked a solid company, earnings should grow over time. And so too will the value of your share or shares. The best part is you get to let someone else run the business. That’s not your job. You are a capitalist after all.

But let’s be real, picking stocks takes skill. You need to understand accounting, read financial statements and have a pretty good sense of the difference between price and value. So how can I get away with saying you don’t need to do anything or know anything? Index funds. All you have to do to be wealthy is buy a Total Market Index Fund, every month. You don’t have to know how to time the market. You don’t need to know which stocks to pick. You don’t need to know when to sell either. And you damn sure don’t need to study accounting. You simply manage your personal cash flow, take the excess each month, and buy stocks. Easy peasy. It’s that simple. Admittedly this does take a level of discipline. Living below your means that is. But hey, nothing worth having is without some element of sacrifice. And would you really cherish the accomplishment later without said sacrifice? Probably not! So buckle down and double down!

We all live hectic lives with our careers, children if you have them and maintaining households. For most people, setting themselves up financially is an after thought. Where do I even begin? It’s all to complicated and risky. And thats why stocks are so amazing. With a simple click of the mouse, or even automatically, you can buy a cross section of American business. Best of all, the best CEO’s in the world will be working hard each and every day to increase the value of your shares. You can have this running in the background. Taking on a life of its own. Making you rich without you even knowing it. In fact, if you never checked it, it would probably be to your advantage!

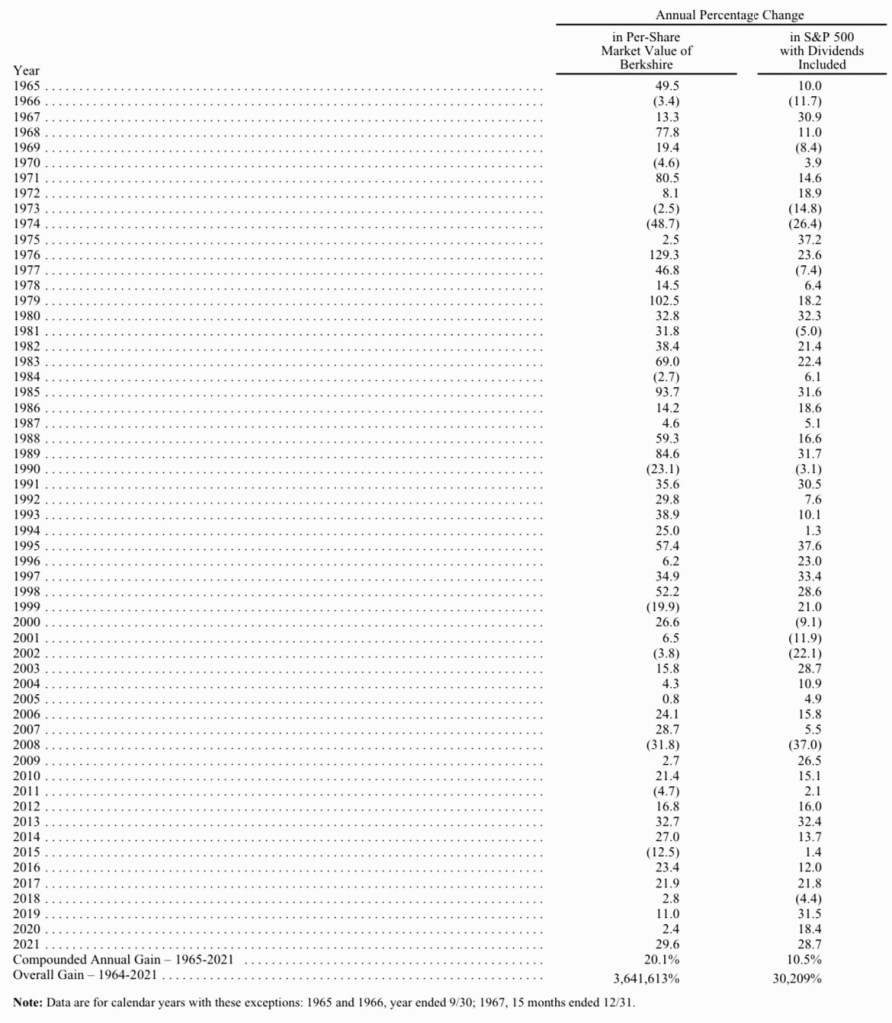

I like to think of someone’s investing career as 40 years. From 20 years old to 60 generally. With that, I’d like to show two different photos. The first one is the returns of the S&P 500 since 1965. The second is the value of your portfolio if you Invested $12,000 a year from age 20 to 60, with a compound interest rate of 10.5%, which is what the market has done since 1965 on average according to the first photo. Sometimes, being lazy is the right move.

Investing is such a fascinating game. There are so many different schools of thought, different approaches and experts to try to gleam advice from. There is a plethora of gurus everywhere you turn. And they all have one thing in ok common. Everyone tells you that you will make your fortune through ACTIVITY. These activities can range from day trading stocks, flipping real estate, buying and selling options, timing stock markets and many other strategies. They all say you need to be in the game and doing something. These strategies are what I would classify as high risk, high reward. But as I get older, I’m convinced you will make your fortune from INACTIVITY. After all, as I mentioned in a previous post there are two basic rules to investing 1. Never lose money 2. Never forget rule number 1.

Full disclosure, I have not followed this line of reasoning for most of my investing career. But you know what? Sometimes the best lessons are those learned from mistakes. You go through life, try different things, stay diligent and if you learn from your mistakes, you get more polished as time goes on. You become weathered, refined and more efficient. But the key is you have to learn and adapt.

That brings me to the point of this post. My advice to those reading is to be boring. Your investing style maybe shouldn’t be something to brag about at a party? Just my two cents. Boring is probably the ideal approach long term for most people. Be the tortoise. I have read this so many times over the past 15 years, and at 37 I finally understand why this is solid advice.

Over the last three months, I have simplified and streamlined my investments. I have moved out of any stock or fund that requires any kind of thought or decision making. Basically I have adjusted my portfolio to be bullet proof. A no brainer portfolio if you will. And I have to say, it’s been one of the best decisions I could have made. I have become the financial equivalent of a basic bitch.

Being boring is, well boring. I find myself nowadays barely checking my various stock accounts. I go weeks sometimes without checking stock prices, the S&P 500 or even real estate prices. I mean what difference does it make really? With my stocks I am 80% indexed in plain Jane total stock market index funds and S&P 500 index funds. I would simplify even more if I could but some accounts only offer certain funds. With the real estate I own, I hardly check the market value of them. Why would I? I do an analysis once a year and type up a profit and loss statement with a few figures such as return on equity and cash on cash return. And as long as these figures are acceptable, I file it and then go about my life.

This level of boring breeds efficiency. it also strips emotion out of the equation. I know that stocks retain earnings and will reinvest those earnings and increase profits over time. So, I own a Total Stock Market Index fund to remove any decision making and spread out my risk. I don’t need to think, to stress or be influenced by market moves. Which could easily coerce me into making costly mistakes. I don’t need to worry if the mutual fund I picked that has a certain strategy was a smart move or if the stock I picked will turn out ok. I just own every stock. And I just keep buying. Consistently. Whether the markets are up or down, to eliminate the element of trying to time the market. You see, boring is a superpower in many ways. And it all but guarantees you follow the two rules of investing mentioned above.

The epitome of boring is Warren Buffett. 99% of his wealth is in Berkshire Hathaway Stock, to the tune of 380k class A shares. Berkshire is not very well known or understood. But I would argue it is a boring company/investment. Buffet’s main job is allocating the capital that Berkshire retains into more businesses and or marketable securities, with the goal of earning more as the years go by. But, he famously missed the dot.com bubble by avoiding any and all internet stocks. In fact, he was laughed at and mocked in the late 90’s as having lost his touch and for being way to old fashioned for such a new tech centric economy. He famously gave a speech in 1999 in Sun Valley Idaho in front of a who’s who of business and tech icons deriding the tech stocks as being wildly over priced. You see, Buffett has always invested in very boring and very predictable companies. To him stability is gold. And that has been his genius. He sticks with what he knows. A famous quote from Buffett at his shareholder meeting in may of 2001:

“We have embraced the 21st century by entering such cutting edge industries as brick, carpet, insulation and paint. Try to control your excitement.”

Suffice it to say, Buffett is boring. Over the last two and a half years, fanciful IPO’s and SPAC’s have brought a level of excitement and capital to Wall Street not seen in decades. Buffett on the other hand chose to hold, cash. To the tune of 145 billion. While everyone else was focused on activity, Buffett focused on inactivity. He did nothing. How did this work out for him?

Remember, investing is kind of like baseball with no called strikes. You don’t have to swing. You can sit at the plate forever and do nothing. And when you do swing, you don’t need to swing for the fences every time. Singles and doubles will produce a satisfactory batting average over the course of your investable career. Think batting average( compounding rate) not home run count.

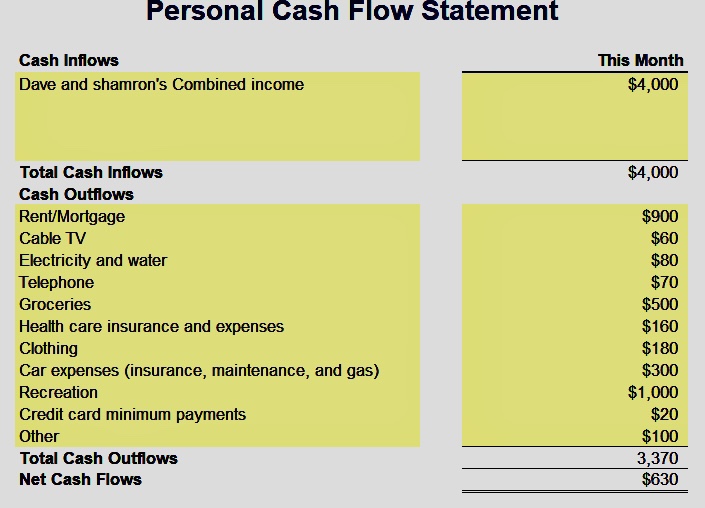

I often get asked, what is the ONE thing I can recommend to help someone with their finances. After hearing a range of problems over the years, my answer is ALWAYS understanding your cashflow. While it certainly isn’t the only thing you should do, it is definitely the first thing and probably the most important. Cash flow is to personal finance as aloe vera is to basically all ailments, being nature’s most powerful natural healer. As such, all problems with money start and end with cash flow. It’s true if you are talking personal finance or business and investments. Understanding the relationship between cash coming in and cash going out is foundational. This cannot bet skipped or done half ass.

So how do you start tracking your cash flow? Brace yourself… keep every receipt or somehow record what you spend money on! And this is your total spending not just your bills. If you give someone a quarter, record it! Ha! No but seriously. It needs to be dead on balls accurate (My Cousin Vinny reference) for you to have confidence in your monthly figures. I also categorize things I’d like to track. For example, food, gas, miscellaneous, entertainment, travel & gifts. This embraces that old adage of what you keep track of you naturally improve. And by improve I mean get more efficient in your spending. Cutting waste, and determining what is truly important and what isn’t. And how that spending is fitting into your long term financial goals.

When I started out I decided that there was a ton of ridiculous Americanized fancy pancy wasteful spending going on. Things that added no lasting value and or happiness to my life. We get sucked into this idea that we work hard. And spending money on things is a natural byproduct of this and we deserve it like a birth right. I was a bit extreme with this early on. I basically didn’t buy anything I “wanted” for years. I bought things I needed of course, like new running shoes yearly, and other things like that. But never just because I wanted it. As I get older and I’ve accomplished some goals financially, i’ve learned it’s ok to every now and then buy a want. Especially if it has lasting value. I recently bought TWO pair of Oakley sunglasses. One for casual every day wear and boating and one mainly for running and outdoor fitness. But these are things I will use every day for a long time. And I have to say they were well worth the money. I love running in them.

I think the key with “want” spending is to avoid impulsivity. Also to scrutinize your spending to see if it improves your life, has lasting value and adds happiness for long periods of time. Avoid the sugar high spikes off happiness that impulse shopping provides.

Ok ok ok, this all sounds simple and easy. If it were that easy then why doesn’t everyone do it? This question is one I think about often. And I don’t really know. If I told you all you had to do was rub aloe on your arm every night before bed and you’d be healthy forever, everyone would do it. Tell people to keep a record of every penny earned and spent and they look at you like you have two heads. The following is an example..

Sometimes I think people doubt I actually do that every month. I suppose it is a lot to do at first. That is until you get used to it. I’ve been doing that for over a decade actually. Month after month. My job is to make sure I have more money come in than go out. And I will do whatever I have to, to make sure of that. It’s that simple.

When I tell people this they start blurting out estimates and ranges. “I spend about 650 on food and 300 on gifts” etc. This is it NOT going to work.

You need to have full accountability. Like you were running a business. Imagine. If every month and therefore every year you knew exactly where all your money went. To the penny. Even more important, you knew how much you spent relative to how much you made. How empowered and in control you would be! The secret to getting ahead is to build the gap between the income and the expenses. And then take that gap and set yourself up financially. But there has to be a gap. Month in and month out. The only way to be sure of this is to keep track. Otherwise you will naturally start to say crazy things like we can afford this that and a third. Spending all the way up to your income. And then the gap is gone. You are now treading water financially.

Do your current and future self a solid and build your gap between income and expenses. Do this by keeping track of your expenses like a religion. Your life will take so many positive steps forward and it will be so much easier. You will be in full control of your finances. Done right and you will have thousands in extra cash every month to pay down debt and later invest. You will be stunned how powerful this is over time. How simple your financial life can be.

Let me give you an example from my own personal situation that will demonstrate how powerful knowing your cash flow is. I have three homes. Two single family rental properties and my primary home. I just replaced all three roofs with 5V Metal. Total cost was $49,040. I don’t have that kind of cash sitting around. Strategically. Better to have it invested. But, I have two lines of credit at low rates. A Home Equity Line of Credit & a credit line against my brokerage account. Both are variable rates. But much lower than a credit card because they are collateralized. In fact, they are cheaper than a mortgage currently. Now using this kind of debt may seem daunting. Admittedly I had anxiety at first as well. But then I realized how much data I have to analyze to determine my expected pay off time. And this alleviated my worry.

I averaged out my free cash flow over the past two years. $4,372 a month is what I averaged, after of course maxing out my 401k. So while still contributing the most I can to my retirement, I still had plenty of cash each year to work with. Suddenly this became an 11 month problem. ($49,040/4,372=11). Ahhhhh the power of knowing what you spend. Been sleeping like a baby every since. And! Now my biggest capital expense at each property is complete. Should be smooth sailing from here.

Now imagine if I was barely squeaking by each month, spending right up to what I made with no accountability and no free cash. I’d be very discouraged and this would be a mounting problem.

Unfortunately, If you don’t have full accountability, you will spend most of what you bring in or possibly even more than you bring in. Cash will dwindle down, forcing you to use credit, refinance your house, take from retirement accounts or even borrow from others when expensive things happen. Imagine a life where you have $8,500 a month coming in on average and $2,500 being spent. This is equivalent to financial angel handing you $6,000 solely to put aside to build your financial empire. Your life expenses have been paid from the $2,500.

Only thing is, it HAS to be used to build your financial future. For example, to pay off debts, build college funds for your children, pay off your house or cars etc. and hopefully build assets once the debt is cleared up. If you start to squander it on useless consumer items the angel takes this “future” building money away. The debt comes back slowly and you backtrack. Fortunately, you don’t need an angel, at least not in this context. You just need to understand how much you spend relative to how much you make.

Just because one company’s stock price is cheaper than another’s does not mean that the company is smaller or worth less. Personally I pay very little attention to the share price. I mean what does it really tell me when you think about it? Doesn’t tell me a damn thing about what the business is worth.

Let’s look at two real companies. WD- 40 Company. That little spray bottle of lubricant everyone has in their garage. The share price is 204.55 currently. Berkshire Hathaway’s B shares are 271.96. Berkshire is a conglomerate that owns many different companies. A holding company if you will. Now, what can you really infer from looking at these share prices? Not much. Sadly, people do it all the time. They know not what they say. Here are a few examples you hear during amateur hour..

“The shares are only 20 dollars they are dirt cheap!”

“The shares are 1000 dollars it’s way to expensive!”

“Im going to wait until after the stock splits and then buy it so it will be cheaper.”

These statements make no sense to the investor. They are the words of someone who doesn’t understand what they are doing. If you follow this line of reasoning you will surely get a poor result relative to the market over time. Moral of the story..understand what you own.

Unfortunately for some insane reason when a company gets broken up into tiny pieces and you have the ability to buy those little pieces every day, people lose sight of what they own and go bat shit crazy. Disco balls come down, cool lights start flashing and the booze starts flowing. Everyone is having a famously good time, then the morning after happens and everyone just wants to forget the bad decisions they made. Ahh the good old college days.

But we are investors right? We know what we own. We will have zero regrets! We look at each share as if it were the whole business. Warren Buffett famously said “investment is most intelligent when it’s most business like.”

A true investor would want to know the number of shares outstanding and the net earnings. Only then can we can start to paint the picture of what we are looking at.

WD-40 Company

204.55 Share Price

13.6m Shares

2.79b Valuation

85.8m Pre-Tax Earnings

Berkshire Hathaway

271.96 Class B Share Price

1.47m Shares (A & B)

597b Valuation

102b Pre-Tax Earnings

Now you have a much better preliminary picture of what you are analyzing. See the significance? (Berkshire has a unique capital structure with A & B shares. The A shares are roughly 400,000 a piece. For this reason they don’t have many shares outstanding.)

Knowing these numbers helps you to paint the picture of what you own. Comparing the share price alone we can reason they are similarly sized enterprises. However, Berkshire is over 200 times the size of The WD-40 Company. And while the share price implies that WD-40 is cheaper, Berkshire is much cheaper relative to the earnings of the company. You are getting much more bang for your buck with the more expensive stock. In fact WD-40’s price is 41 times earnings, while Berkshire’s is only 7.43 times. Clearly Berkshire is cheaper when you think about it like an investor. Price is what you pay, value is what you get.

An investor is concerned how the underlying business performs over time. Ask yourself, if I purchased the shares at the current price, what am I actually paying for the entire company? The whole point of investing your capital now is to ensure you get more back as you go along. How much will the company produce on a net basis relative to what I paid? Is that a satisfactory return? What’s my competition and is the company solvent? Most importantly, will the company deliver enough cash soon enough to make it a sensible investment relative to prevailing interest rates.

For example, If you could take much less risk on a 10 year government bond and get a higher return, why take on the risk of owning stock in a company where the return isn’t so certain?

Make sure it’s a satisfactory return relative to the purchase price of the entire enterprise. And understand the limitations of the per share price and what it tells you about valuation. Your future self will thank you.

It’s easy to see how investing in the stock market could be considered gambling with your money. It’s like going to Vegas right? You take a dollar amount that you’re comfortable losing and hope that you make the right bets to turn it into more. You might even think that Vegas is safer. At least in Vegas you can win or lose based on your own skill depending on the game you play. This idea that stocks are this crazy gamble and too risky keeps people on the sidelines. In reality the stock market has been one of the biggest wealth creators the world has ever seen. In order to capture that wealth generation you need perspective, understanding and the right approach. Once you have these, you can basically build huge amounts of wealth with basically little to no risk at all. Yes I said it.

First let’s be honest, there is certainly gambling going on with stocks. There always has been. It’s kinda like a community pool, everyone is welcome. Options, selling short and credit default swaps are but a few methods investors use to speculate in markets. These professionals try to make money on short term swings in the markets. These methods can be incredibly profitable if they work. But this is incredibly advanced, and probably should be avoided for anyone who isn’t a professional. Hell, even professionals should avoid these types of trades most of the time. I like to think about investing like baseball. Over my investing career, how do I achieve the highest batting average (compound interest rate)? I don’t need to hit home runs and swing for the fences to be effective. I need consistent singles and doubles. And more importantly, I need to never strike out. So, over the course of my career I have a nice solid average. They say there are two rules of investing. 1. Never lose money. 2. Never forget rule number 1.

Unfortunately, everyone has a story of some huge stock win they had, or your friend down the street who is making a fortune day trading yada yada. And this entices people to start swinging for the fences. Most likely, none of them will outperform the market over time. They may do it for a year or so, but over the course of their investing career they likely will not. Statistically, 78% of mutual funds underperform their benchmarks over a 20 year time frame. And those are professionals! Outperforming markets is a very hard. You can try to dance in and out, time the market, buy the dips and so on. But an honest appraisal of your performance in 30 years would likely show you did worse than the market. And that would be a crappy feeling.

But! If you just consistently buy every month you would have gotten very rich over time by simply owning a boring S&P 500 index fund, as this table below shows. A $5,000 dollar investment with no further investment would have grown to $2,208,355 with a 10.5% compound rate since 1965, which is what the S&P 500 delivered. But as the table below shows, you would have had to deal with some extreme volatility. Understanding what you own and having a long term view helps to calm the nerves.

S&P 500 Returns With Dividends Reinvested:

1965 10.0

1974 (26.4)

1994 1.3

1998 28.6

2002 (22.1)

2008 (37.0)

2021 28.7

Compounded Average Annual Gain 1965-2021 10.5%

What Is A Stock, Anyway?

Before you can be comfortable with the stock market, you have to know what a stock is. A stock is not just an arbitrary number that bounces up and down on a chart based on a series of random events. In fact, when you own shares in a company, you own a claim claim check on the net assets of the company now and on the future earnings of the company. A great illustration of this is the NBC show “Shark Tank.” In the show, people who need capital pitch their businesses to a group of investors to raise capital. So if their company is valued at $1 million, they may ask the sharks for $200k of capital in exchange for 20% ownership of the business. Similarly, when a company needs capital to grow, they offer shares to the public in an IPO (Initial Public Offering). By selling partial ownership to shareholders, they avoid taking out a loan or selling bonds, which are required to be paid back with interest. Upon the IPO, a one time transfer of shares is exchanged to the public at a stock’s par value. On IPO day, the difference between the par value and what the shares start trading at is the amount of money that will be raised. It’s a one time transaction. Subsequent trading is then between investors.

It is important to note that each company has a different amount of shares outstanding. This is important because just because a share price is higher than another, this does not mean it’s more valuable. The Value of the company is determined by the share price multiplied by the number of shares outstanding. Example: Washing Trust Bancorp Inc. is a publicly traded company. At present it has 17.35m shares outstanding. Share price is 49.91 presently. (17,350,000 shares * 49.91 per share price= market value) So the whole company is worth 870m essentially. Hypothetically, if you owned 1.73 m shares, then you would own 10% of the company. 9.2m of the 92 million they earned last year would be yours. This is to help illustrate what you really own. You own a piece of a business when you own stocks. Whether you own a small piece via stock, or the whole company, your approach to investment should be the same.

Minimizing Your Risk

What are the Four main risks to investing in the stock market?

Buying At The Wrong Time

Short Term Thinking

Buying The Wrong Stock

No consistency

How do you basically eliminate all four risks? Dollar Cost Averaging (DCA) into a broad based market indexconsistently over a long period of time!

Buying At The Wrong Time: Dollar Cost Averaging is buying into the market consistently, whether share prices are up or down. The benefit of DCA is that it lessens the impact of market fluctuations overtime, all but eliminating the risk of timing the market wrong. Imagine you invest $500 into the market EVERY month. In January, the average share cost you buy is $100, so you’ve bought 5 shares. Then, in February, the average share cost jumps to $150. Now that $500 only bought 3.33 shares. However, in March the average share price is only $50. That means for that same $500 you’ve bought 10 shares. By consistently investing, you’re minimizing the impact of swings in the market. You are also forcing discipline. You are buying less when things are expensive and buying more when prices come down. This all but ensures a satisfactory result over time.

Short Term Thinking. The stock market is a long term game, you need to be willing to leave it in for at least 10 years. Here is an illustration to show just how long term you need to be when thinking about the stock market. The 17 long years between 1964 and 1981 stocks went nowhere. That’s a long time. Stocks were simply unfashionable. But over the course of the century they went up 17,000%. It’s important to keep a long term perspective.

Dow Jones Industrials

Dec 1964: 864

Dec 1981: 865

Dec 1900: 66

Dec 1999: 11,467

Buying The Wrong Stock. The only reason to buy an individual stock is to try to outperform the market. I mean think about it. You always have the default option of owning a broad based market index. It’s not exciting or flashy. You won’t be bragging to your friends about this hot new Total Market Index fund you bought that’s making you rich. But we know from research that outperforming these indexes over time is futile. So why not take that default option? Personally my largest holding in my portfolio is ITOT, which is a Total Market ETF. I don’t worry about buying the wrong stock. I just own all of them. Simple. I keep is simple as they say. Full disclosure I do own a few individual stocks. This is more the business nerd in me more than anything else. I consider myself a part owner of these companies and enjoy reading the quarterly and annual reports. This is more for enjoyment than trying to beat the markets.

No Consistency. I don’t have any special advice here. This is pure grit. Make it a priority. Pay yourself first. We live in a highly consumer driven economy and society. You can’t possibly be happy without the latest and greatest of everything. To that I say, keep it simple. Keep your life simple. Do some stuff yourself. Hang on to your cars and tech devices. Make stuff last. Lower your consumer footprint. Your future self will thank you tremendously. From my personal experience, you will be happier when you stop relying of “things” to make you happier. Just my two cents. On this topic, here is a great quote from the man himself Mr Money Mustache, one of the top personal finance bloggers..